France’s E-Invoicing Mandate: What It Entails, What It Means for You & How to Ensure Compliance By 2024

B2G (business-to-government) e-invoicing has been mandatory since 2017, and soon, the same will be required of all B2B (business-to-business) transactions as well.

On December 28, 2019, the French government passed Art. 153 of France’s Finance Law 2020, making e-invoicing mandatory for all domestic B2B transactions starting in 2024. All business entities will be required to accept electronic invoices, regardless of their size. This mandate will gradually be applied between July 1, 2024, and January 1, 2026, according to a schedule and terms set by decree depending on company size and sector of activity.

Is your business prepared to be fully compliant by the 2024 deadline?

Here’s a breakdown of what the mandate requires of B2B transactions and how your organization can ensure total compliance with France’s Finance Law 2020.

Why Art. 153 is a good thing for businesses

France’s Finance Law 2020 is based on four main objectives: boosting competitiveness, combating VAT fraud, increasing business efficiency and simplifying VAT returns. That sounds like all good stuff for your organization, right?

Right!

For companies that have been slow to transition to e-invoicing, this mandate is almost a blessing in disguise. By making e-invoicing mandatory for businesses of all sizes, now everyone can capitalize on the benefits it delivers.

Key e-invoicing benefits:

- Reduced processing costs

- Faster payment thanks to quicker and mroe efficient invoice sending

- Improved visibility on internal processes and team performance

- Compliance with regulations and customer/supplier relationships

- Reduced environmental impact

- One unique platform to digitally transform source-to-pay (S2P) and order-to-cash (O2C) cycles.

Sending and receiving e-invoices

Requirements for sending e-invoices

There are three key dates that are important to remember when it comes to France’s e-invoicing implementation. Businesses will be required to issue e-invoices according to this schedule:

July 1, 2024: Large enterprises (5,000+ employees and/or 1.5B+€ in sales revenue)

January 1, 2025: Mid-Market enterprises (250 to 5,000 employees and/or 50M€ to 1.5B€ in sales revenue)

January 1, 2026: SME & VSB (-250 employees and/or -50M€ in sales revenue)

Requirements for receiving e-invoices

Companies subject to VAT in France need to be able to receive e-invoices in the mandated formats UBL 2.1, UN/CEFACT CII, and Factur-X as of 1st of July 2024. Make sure your AP solution can receive and process the permitted formats.

Processing invoices

The e-invoicing exchange model allows for three different transmission options:

- Both parties use the public invoicing portal, Chorus Pro. Supplier enters their invoice Chorus Pro, which then delivers it directly to the end customer.

- Only one of the two parties (supplier or buyer) uses a private registered platform. For example, if a supplier uses a private registered private platform: the supplier uses their own platform to submit their invoice to Chorus Pro, which then delivers it directly to the end customer.

- Both parties use a private registered platform of their choice. Supplier uses their own platform to transmit the invoice data to Chorus Pro to report it. And simultaneously, the supplier’s platform delivers the invoice to the end customer’s private registered platform.

Reporting requirements

One of the main objectives of e-reporting regulations includes fraud detection.

E-reporting describes the requirement to report invoicing data and payment information for transactions carried out electronically within France by individuals (B2C) or foreign operators (international transactions), such as:

- Sending of invoice data and related accounting items

- Transmission of these items via Chorus Pro for both buyer and seller

- Verification of tax information by tax authorities

The French government, therefore, requires e-reporting for three types of flows that had not previously been impacted by the e-invoicing statutes:

- B2B international transactions

- B2C transactions

- Intra-community acquisitions

- Acquisition of services outside the EU

- Cash receipts when VAT is due

Formats and platforms

The public invoicing platform Chorus Pro will provide all required tax information to the DGFIP by extracting the necessary information and performing reviews on transmitted invoices. Businesses will be able to manually enter invoices, view them and their associated processing status and archive them online.

The Agence pour l'informatique financière de l'Etat (AIFE) will create a business directory so that invoices can be correctly distributed via a common reference system. Three reception grids are possible: the business identification number (SIREN), the unique French business identification number (SIRET), or a routing code (e.g., service code).

Invoicing data may also be exchanged via private platforms. These platforms must have the ability to extract the data from the invoice and confirm the existence of the required mandatory information (in the same conditions as Chorus Pro). The registered private platforms will also be in charge of updating the business directory on behalf of their clients.

Transmissions

Invoices must be issued in structured or hybrid format (structured format + PDF). Any platform will be able to receive invoices in three different mandatory formats: UBL, UN/CEFACT CII (structured formats) and Factur-X (hybrid format). Simple PDF invoices will no longer be accepted, although allowing for exceptions within a transition period. E-invoicing platforms should be able to generate hybrid formats consisting of structured data and a readable PDF from a simple PDF file.

New mandatory information has been added, creating a list of more than thirty data items to be transmitted to the tax authorities (twenty or so as of 2024 and eight in 2026, to allow for a more a more comfortable transition for businesses).

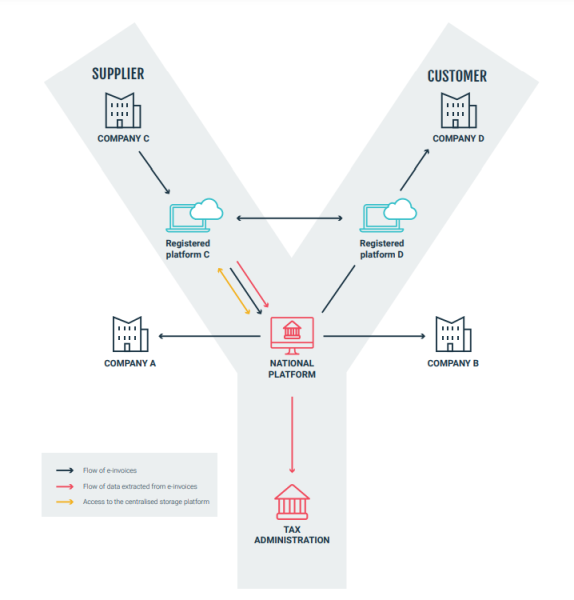

Y-scheme model

The DGFIP report recommends a Y-scheme model that would allow 3rd party platforms to transmit e-invoices to recipients without passing through the public invoicing portal called Chorus Pro. The Y-scheme model was chosen because it allows businesses to continue to work within their accustomed structures and with their existing e-invoicing providers, while also conforming to the new regulations. It looks something like this:

Central business directory

As part of the invoice reception process, a central business directory will be set up so that everyone has the same reference system to ensure that invoices are correctly routed between platforms. This directory will be used for B2B and B2G regulations and will include:

- The list of companies and routing information related only to the receipt of its invoices

- A routing code to identify the chosen platform (a unique code for each routing possibility)

The business directory will be updated by:

- Chorus Pro only for the creation and termination of companies

- The company if it uses Chorus

- The registered reception platform, if the company uses a registered platform to receive its invoices

How Esker can help ensure total compliance with the 2024 mandate

Esker helps companies deliver e-invoices in compliance with all the unique specifications of European countries. This includes processing any format (e.g., PDF, UBL, Facturae in Spain, Fattura-PA in Italy, etc.), communicating with PA platforms (including PEPPOL) to send e-invoices and provide status updates, and providing e-invoice archiving that’s compliant with the EU Directive and regulatory frameworks.

Accounts payable automation

Esker’s Accounts Payable solution enables companies to eliminate manual tasks associated with invoice processing. Thanks to data capture features, automated processing and an AI-based electronic workflow, your cash management is simplified and more efficient.

All your invoices are processed regardless of format or reception channel (e.g., mail, email, EDI, etc.). You also benefit from customizable KPIs and on-the-go review and approval functionalities

Accounts receivable automation

Esker’s Accounts Receivable solution automates the delivery of customer invoices via any media (e.g, paper, e-invoices, EDI, portal, Chorus Pro platform, etc.), in compliance with existing regulations. Manage invoices electronically with real-time visibility into invoice delivery status thanks to Esker’s single and user-friendly interface.

Your customers can view, pay or dispute an invoice, as well as communicate directly with your teams via an integrated messaging tool on Esker’s portal, accessible 24/7. Esker makes your life easier, simplifies exchanges and saves you precious time.

Want to know more about leveraging automation for efficiency and compliance with e-invoicing mandates? Download this insightful ebook and keep learning!

Taylor Bucher

As a Copywriter at Esker, Taylor uses her creative writing experience to write engaging marketing content that educates audiences on the benefits of automated business processes. If she’s not in the office, you’ll most likely find her exploring hiking trails, guessing the breeds of dogs she sees on the street and then asking the owner to see if she’s right, or catching a concert at a local music venue.