Non-Financial Sustainability Reporting: Everything You Need to Know About the EU CSRD Requirements

Applicable starting January 1, 2025, for the 2024 Financial Year, the Corporate Sustainability Reporting Directive (CSRD) sets new standards and requirements for non-financial reporting. This European Union directive upon the EU’s Green Pact - a commitment to establishing carbon neutrality by 2050. Which businesses are affected, and how can they adhere to the new regulations? And what is the predicted impact on their performance evaluation?

The CSRD: A framework for extra-financial reporting

The (CSRD) is a new directive introduced by the European Union. Its aim is to establish a new framework for extra-financial reporting by businesses on their environmental, social and governance (ESG) impact. The basic aim is to include the notion of corporate responsibility into the analysis of company performance. Signed and passed in 2022, the CSRD came into effect on January 1, 2024.

Objectives: Tightening regulations

The CSRD replaces a previous directive, the Non-Financial Reporting Directive (NFRD), which already imposed a CSR declaration on a number of companies. Four objectives guide the CSRD:

Increase the completeness, accuracy and reliability of the information collected

Extend the reporting obligations to more businesses

Raise the awareness of environmental impact businesses have, including ESG risks

Standardize balance sheets across the EU

From NFRD to CSRD: What are the differences?

There are 5 major differences between the CSRD and NFRD:

1. Its scope of application - gradually applied, it will eventually cover more than 50,000 companies in Europe, compared to previously 11,000 for the NFRD

2. Its detailed European declaration standards

3. A more exhaustive analysis of the company's non-financial impacts

4. An analysis of the risks created by the company, in addition to those of risks incurred

5. Audits by an independent body, rather than in-house

Which businesses are affected by the CSRD?

The companies impacted by the CSRD directive include:

- European structures that meet certain criteria such as number of employees, sales and balance sheet totals

- SMEs listed on European markets that meet specific thresholds

International companies with net sales in excess of €150 million in the EU are also affected by this directive.

1. Mid and large-sized European companies

The European companies impacted by this new reporting obligation are those that meet at least 2 of the 3 criteria:

- Companies with at least 250 employees

- And/or companies generating sales in excess of €50 million

- And/or companies with a balance sheet total in excess of €25 million

SMEs listed on European Markets

Small and medium-sized enterprises (SMEs) are also affected if they meet at least 2 of the following 3 criteria:

- SMEs with more than 10 employees

- And/or SMEs generating over €700,000 in sales

- And/or SMEs with total assets in excess of €350,000

Non-European companies

International companies that deliver goods or sell services within the EU and have net sales of over €150 million will also have to publish data on the sustainability of their activities.

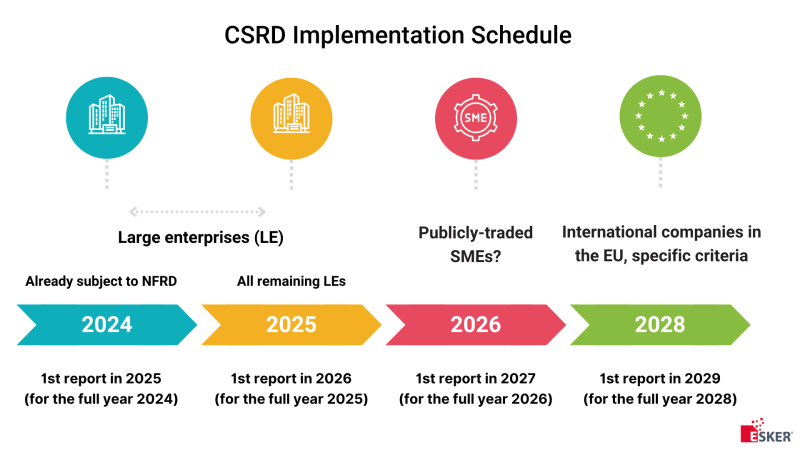

What is the CSRD implementation schedule?

With the exception of international companies, businesses are subject to the CSRD when they meet at least 2 of the 3 criteria listed.

January 1, 2024

2025 (for FY 2024)

Large companies already subject CFRD

- Employees ≥ 500

- Sales ≥ €40 million

- Balance sheet ≥ €20 million

January 1, 2025

2026 (for FY 2025)

Large enterprises that meet specific creiteria

- Employees ≥ 250

- Sales ≥ €40 million

- Balance sheet ≥ €20 million

January 1, 2026

2027 (for FY 2026)

Publicly traded SMEs

- Employees ≥ 10

- Sales ≥ €700,000

- Balance sheet ≥ €350,000

January 1, 2028

2029 (for FY 2028)

Multinational businesses operating in the EU and meeting these two conditions

- Their European business generates over €150 million in net sales.

- They have a local subsidiary.

ESRS : What are the CSRD indicators?

The CSRD establishes the new European Sustainability Reporting Standards (ESRS) for businesses for the preparation of the annual balance sheets. Established by European Financial Reporting Advisory Group (EFRAG) and adopted on July 31, 2023, the 12 key points correspond to one of the three ESG strands. For each axis, the company must present the impacts (emissions, commissions, etc.) and the measures put in place to address these.

Environmental impacts (E)

- Climate change

- Pollution

- Aquatic & marine resources

- Biodiversity & ecosystems

- Resource use & the circular economy

Social components (S)

- The company's workforce

- Employees in the value chain

- Consumers & end users

Governance (G)

- Ethical business conduct

What does double materiality in the CSRD refer to?

What is simple materiality?

Originally, accounting information was considered material when it reached a so-called "materiality" threshold, beyond which it had a direct impact on the company's economic decisions. Today, the term is used to describe an organization’s ESG policies, enabling them to assess and prioritize the importance of the various ESG issues.

Double materiality & the CSRD

Like simple materiality, "double materiality" aims to evaluate the significant information that can influence financial decisions relating to the company. The concept of simple materiality (outside-in) is combined with the complementary notion of impact materiality (inside-out), which focuses on the influence of the company and its activities on the environment and society. This is a central CSRD tool for identifying the issues that should, by their very nature, be included in the sustainability report because of their strategic importance.

Example: A food company

- Financial materiality ("outside-in") → Poor harvests due to climate disruption impact the company with supply chain difficulties and higher prices.

- Materiality of impact ("inside-out") → The company has a mediocre carbon balance: it can pollute through its production activity, but it can also implement decarbonization strategies.

Companies affected by the CSRD: How to proceed?

In view of its broader scope, the CSRD requires a greater number of companies to comply. Preparing for this transition is therefore essential, especially for those who were not subject to the previous regulations.

1. Get to know the requirements

First, it's important to analyze the new regulations.

- What are the new requirements?

- What is their scope?

- Which departments are affected?

- What actions are needed?

Remember that ESG issues are numerous and interdependent.

2. Implement a dual materiality analysis

Formulating a dual materiality matrix is essential. Achieving the sustainability objectives encouraged by the CSRD involves all business functions. They must also be involved in monitoring and analyzing the company’s ESG policy. Consulting firms offer support services for matrix formulation. They can also be helpful with:

- An improved identification of risks & opportunities

- An informed participation from all departments

Combining the inside-out (impact materiality) and outside-in (financial materiality) analyses will help in:

- Deepening the understanding of sustainability issues

- Providing a global, balanced view of risks & opportunities

3. Analyze deviations

Performing a gap identification based on the company's current state and materiality analysis will enable the formulation of a detailed roadmap to meet future regulatory requirements.

4. Organize data collection

Companies will need to collect and report on a large number of data points (up to 1,200). Anticipating and addressing the composition, collection and reliability of the data is imperative in order to meet the CSRD information requirements.

What are the benefits of complying with the CSRD?

The CSRD aims to facilitate the social and ecological engagement of businesses. Reporting on these factors will have many positive effects, including:

- Enhanced reputation & stakeholder confidence

- Alignment with sustainable development goals

- Easier access to sustainability financing

Investors may fear that CSRD is just another compliance exercise with no real-world impacts. In reality, the directive gives businesses a better understanding of the impacts of the business operations on the environment. These are, however, relevant indicators when negotiating or tendering, for example.

What are the penalties for non-compliance with the CSRD?

Each EU member state sets its own penalties for non-compliance with the CSRD. In France, for example, financial penalties vary according to two scenarios¹:

- Failure to certify sustainability information: The head of the company risks a €30,000 fine and up to two years imprisonment

- Obstructing certification of sustainability information: The head of the company director risks a €75,000 fine and up to five years imprisonment

In addition to these sanctions, other measures can be taken:

- Image sanction: Public publication of the company's name and the nature of the offence

- Regulatory sanction: A cease-and-desist order linked to the offence

- Financial penalty: A fine based on the company's financial situation and the profits generated by the infringement

Beyond legal and financial consequences, non-compliance can lead to reputational damage, and other more wide-ranging consequences including loss of investor confidence, market restrictions and difficulties building and maintaining partnerships.

How can Esker help with consolidating this data?

Esker's expertise in sustainability reporting goes beyond simple data collection. Although Esker solutions do not directly calculate sustainability indicators, they play an essential role in consolidating and managing the data required for accurate reporting. With the Esker Supplier Management, companies can automate supplier ESG questionnaires, monitor the evaluations and ensure compliance with ESG standards, thereby improving supply chain sustainability. Similarly, Esker Accounts Payable extracts energy consumption from utility bills, tracks the company's carbon footprint, optimizes emissions and facilitates advance payments to suppliers, thereby contributing to a more sustainable business model. By leveraging both Esker Supplier Management and Esker Accounts Payable, companies can streamline their sustainability initiatives and make informed decisions in order to reduce their environmental impact.

1 Source: https://portail-rse.beta.gouv.fr/reglementations/rapport-durabilite-csrd